���W�����W֪���ڿ����]J MATH ECON

�r�g��2025��01��24�� ���SCIՓ�İٿ� �Δ���

����������픵�W�����W֪���ڿ�J MATH ECON��ȫ�Q��Journal Of Mathematical Economics���ǔ��W������Ŀ�������Ǿ��w��Ԕ���B�����W�I���ˆT�����酢����

�����ڿ�����ָ�ˣ�

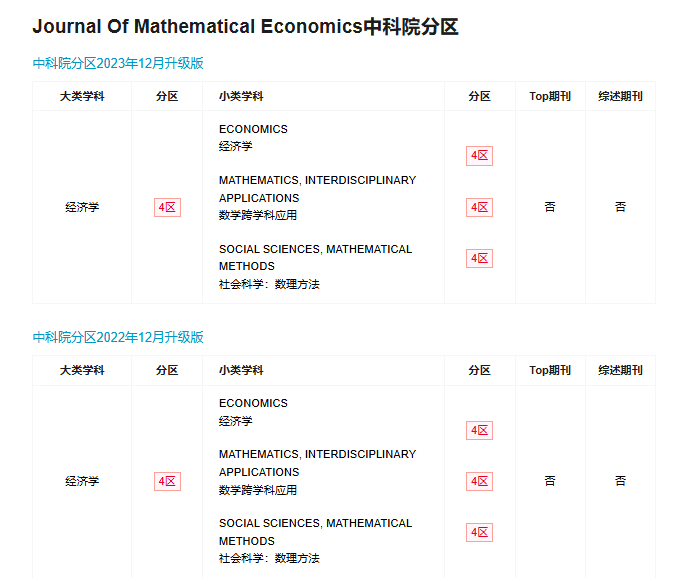

�����Ї��ƌWԺJCR��������W4�^

�����Ї��ƌWԺJCRС������W4�^;���W��W�Ƒ���4�^;����ƌW����������4�^

����Ӱ����ӣ�1

���������ʣ�14%

��������ռ�ȣ�4.62%

����ISSN��0304-4068

����E-ISSN��0304-4068

����J MATH ECONĿ�˺ͷ�����

����ԓ�s־����ҪĿ���Ǟ齛����Փ�����ṩһ��Փ����ʹ����ʽ�Ĕ��W��������_����˼�롣���������@����ҪĿ�˵Ĺ��������W�������µĺ����_���Dz���ġ���Ʒ��횾����挍�Ľ������ݡ�����˼��������Ȥ����Ҫ�ġ��@Щ�뷨�����漰�κν����W�I����κν���˼�����ɡ�

����J MATH ECON�����

������Ҫ�l���\�Ô��W�����о�������Փ�ͽ������}��Փ�ġ�

�������w�^�����W�����^�����W������Փ���Q����Փ�ȶ��������W��֧�I��

�����Ą�����F���M�н�ģ���������A�y�Ą������о���

�����ڿ������c��

�������I�ԏ����锵�W�����W�I��ČW���ṩ��һ�����I�ČW�g����ƽ�_��

������W���ԣ��ں��˔��W�ͽ����W�ɂ��W�ƣ����M�ˌW��֮�g�Ľ����c������

���������ԣ��Ą���Ե��о���������Փ���ƄӔ��W�����W�İlչ��

�������HҕҰ�������ˁ���ȫ����صČW��Ͷ�壬���ЏV���ć��HӰ�����

����Ͷ��ע����헣�

����Փ�đ��߂�������߉�Y���͜ʴ_�Ĕ��W�ƌ����Z�Ա��_ҪҎ�������������όW�g������Ҫ����ѭ�ڿ��ĸ�ʽҎ�������������īI�Ę�ע�ȡ�

�����ڿ���ί���ɆT��

����������

����A. ���߹���

�����������၆��W���S˹��У(�������S˹��У)�� FGV(�����|�ϲ���s��ȱR��У)

�����Ͼ���

����C. Beviá Baeza

�����������ش�W�� �������� ��������

������������

����M. ������

������������W��������

����P. ��Ī�_˹

�����������R���Ӵ�W

����J. Apesteguia

�������������෨������W

����Փ�İ�����

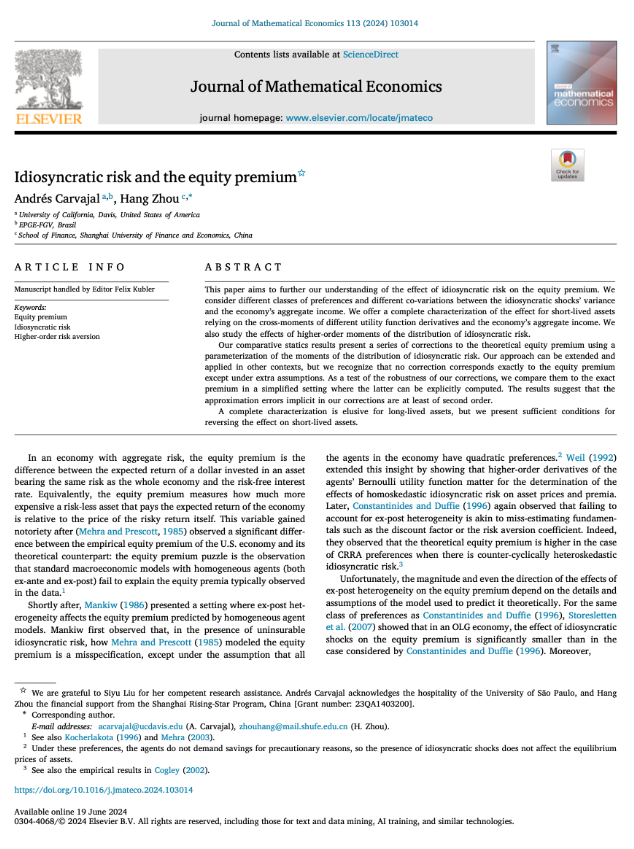

�������ڣ���Ժ�ܺ��ώ��c�����ߵ�Փ�� Idiosyncratic risk and the equity premium(�خ����L�U�c�ə���r)�l���ڽ����W�֪���ڿ� Journal of Mathematical Economics�ϡ�

�������ߺ��飺

�����ܺ����Ϻ�ؔ����W���ڌWԺ�����ڣ���Ҫ�����Ј��^�Y�����О���ڌW���о����ɹ��l���ڇ��Hһ���ڿ�Journal of Economic Theory��Economic Theory��Journal of Mathematical Economics, Real Estate Economics�ϡ�

����Փ�ĺ��飺

����Փ���}Ŀ��Idiosyncratic risk and the equity premium. (�خ����L�U�c�ə���r)

������ �ߣ�Andrés Carvajal, Hang Zhou

�����l���s־��Journal of Mathematical Economics (���������W)

�������ĺ��飺�@ƪՓ��ּ���Mһ�������҂����خ����L�U����Ʊ��rӰ푵����⡣���Ŀ��]�˲�ͬ��͵�ƫ���Լ���ͬ���خ����L�U�c�����w���w����֮�g�ąf����҂��ṩ��һ�����ı��_ʽ���Á�Ӌ���خ����L�U�ͽ����w������֮�g�ąf����ڶ����Y�a�r���Ӱ푡��҂�Ҳ�о����خ����L�U�ĸ��A�،����Y�a���r��Ӱ푡��҂��������خ����L�U�ֲ��ľصą����������������һϵ��������Փ��Ʊ��r�ĽY��������ָ���˱��������Ա�������������һЩ���}�ϡ��҂��Ķ��������Y��ָ�������A�����ѽ��܉�õ��������_�ĽY���������L���Y�a���о����҂��o���ṩһ�����ı��_ʽ�����҂����о��ṩ��һЩ��֗l���������҂��l�F�����Y�a�ĽYՓ�������L���Y�a�в���������

����Ӣ�ĺ��飺This paper aims to further our understanding of the effect of idiosyncratic risk on the equity premium. We consider different classes of preferences and different co-variations between the idiosyncratic shocks’ variance and the economy’s aggregate income. We offer a complete characterization of the effect for short-lived assets relying on the cross-moments of different utility function derivatives and the economy’s aggregate income.

����We also study the effects of higher-order moments of the distribution of idiosyncratic risk. Our comparative statics results present a series of corrections to the theoretical equity premium using a parameterization of the moments of the distribution of idiosyncratic risk. Our approach can be extended and applied in other contexts, but we recognize that no correction corresponds exactly to the equity premium except under extra assumptions. As a test of the robustness of our corrections, we compare them to the exact premium in a simplified setting where the latter can be explicitly computed. The results suggest that the approximation errors implicit in our corrections are at least of second order. A complete characterization is elusive for long-lived assets, but we present sufficient conditions for reversing the effect on short-lived assets.

�����ڿ�������ڣ�

���������~�D�W�g���]�͌������£����YҎ�ɣ����ύ���µ��ڿ��ٷ�Ͷ��ϵ�y�_ʼ��������ϵ�y��B׃����Accept��ֹ���������ڞ�6�������ҡ�

�����ڿ��������ڣ�

���������~�D�W�g���]�͌������£����YҎ�ɣ��Č���ϵ�y��B׃����Accept�_ʼ�����ڿ��پW��ʽ�Ͼ����½�ֹ���������ڞ�1-3�����ҡ�

- �����W�s־Lithuanian Mathematical Journal

- ���ôWͨ��CAN MATH BULL��sci3�^�ͷ�ֵ�ڿ�

- ���W��������top�����]COMPOSITIO MATHEMATICA

- Ӌ�������W���I�����ڿ�Econometrics Journalһ�^����ǰ20

- ���WEXPERIMENTAL MATHEMATICS�օ^�ߣ�Ӱ����ӵ�

- mdpi��Ӱ����ӵ��ڿ�

- 10����ÿ�Ľ����W������HӢ���ڿ����]

- ���W���I�Tʿ���I��Փ�ĵ�Ҫ��

- MDPI���µ���ľ�����I���ڿ�

SCI�ڿ�Ŀ�

���T�����ڿ�Ŀ�

SCIՓ��

- 2025-01-26�����W�s־Lithuanian Mathe

- 2025-01-254��������ԃr��SCI�ڿ����]��

- 2025-01-24���W�����W֪���ڿ����]J MATH E

SSCIՓ��

- 2025-01-25ͨ�^�ʸ�!���]6�����ðl��ˇ�gSS

- 2025-01-22�Z�Ԍ��I�о����m��Ͷ�������ڿ�

- 2024-12-24�����ssci�ڿ���ȫ����������ss

EIՓ��

- 2025-01-26ei���hͶ�嵽���Ԕ���^��

- 2025-01-24�������eiՓ��ˮƽ

- 2024-12-282024.11��EI�ڿ�Ŀ䛣�����18��

SCOPUS

- 2025-01-24scopus�l�����¸�ʽ��ָ��

- 2024-11-19Scopus��䛵Ľ���������ڿ�

- 2024-05-29scopus�����Щ������ڿ�

���g��ɫ

- 2024-11-22���H�����ڿ��l��Փ�đ�ԓ��ʲô

- 2024-11-22���H���Ľ̎����ڇ��H�����ڿ��l

- 2024-11-22���H�����ڿ��u�Q���J��

�ڿ�֪�R

- 2025-01-24�ڿ��κˡ��p����ʲô��˼

- 2025-01-23���н�ͨ�lչ���P�����m��Ͷ����

- 2025-01-21�������w�W�����ڿ��ϼ�

�l��ָ��

- 2025-01-25Փ��Ͷ��ǰҪ�z����Щ����?

- 2025-01-24�t�W�о����Į��IՓ���x�}�v��

- 2025-01-23�����Ļ������Փ���īI39ƪ